The Government of every country needs funds to spend on the economic and infrastructural development of the nation. These funds are sourced from the citizens of the country in the form of taxes. Taxes are, therefore, compulsory payments done by the residents of a country to their Government for meeting the cost of basic public amenities.

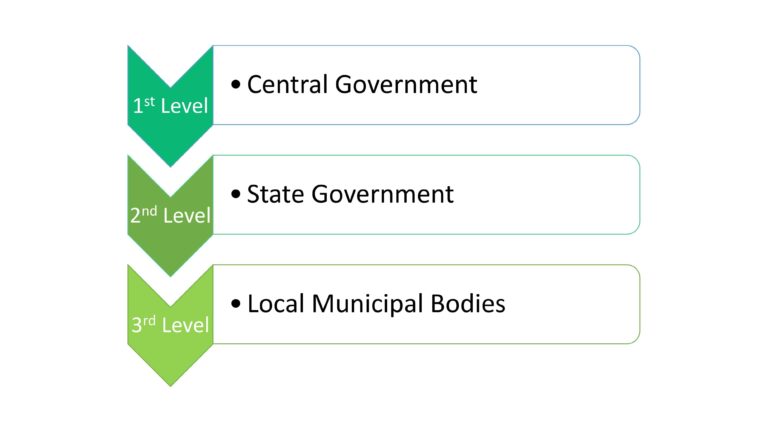

In India, The Constitution has given the Government the right and the authority to collect taxes from Indian residents as well as non-residents earning income in India. India has a three-tiered tax structure which is as follows

Types of tax in India

In India, there are, broadly, two different types of taxes.

- Direct tax

Direct tax is one that is levied directly on an individual and paid by him/her to the Government. The income tax that you pay on your income is a common example of direct tax. You cannot avoid paying direct tax if you earn an income in a financial year and the income exceeds the specified threshold limits.

- Indirect tax

As the name suggests, indirect tax is a type of tax that is indirectly levied on an individual. The tax is, usually, levied on goods and services and forms a part of their cost. Thereafter, if you purchase such goods and services, the tax liability passes onto you and you pay tax on it which has been included in the price. You can avoid paying an indirect tax if you don’t buy the goods and services on which the tax has been levied.

GST is a very common example of indirect tax that you have to pay if you buy goods and services on which GST is levied.

Types of direct tax

Both direct and indirect taxes are further subdivided into different types. The types of direct taxes which are applicable in India are as follows

- Income tax

This tax is applicable if an individual or a Hindu Undivided Family (HUF) earns an income in a financial year. Income tax is applicable as per the provisions of the Income Tax Act 1961. If the income earned by an individual or a HUF exceeds INR 2.5 lakhs, income tax would be payable on such an income. In the case of senior citizens, aged between 60 and 80 years, however, the threshold limit for income tax is INR 3 lakhs. For super senior citizens aged 80 years and above, the threshold limit is INR 5 lakhs.

- Corporate tax

Corporate tax is a type of income tax paid by a company, whether domestic or international (operating in India), on the income that it earns in a financial year. It is also governed under the Income Tax Act, 1961. Corporate tax includes other taxes as well which are as follows

| Types of tax | Meaning |

| Minimum Alternate Tax (MAT) | Companies that prepare their accounts as per the Companies Act, 1956 and have a zero tax liability are required to pay MAT |

| Fringe benefits tax | If companies pay fringe benefits to their employees, like paid accommodation, transportation, etc., they have to pay tax on the economic value of such benefits |

| Securities Transaction Tax (DDT) | If a company does a taxable security transaction, STT would be payable on the value of such a transaction |

- Capital gains tax

If you have a capital asset and you transfer the asset and earn a profit on such transfer, the profit would be called a capital gain. This capital gain would, then, form a part of your income and attract a capital gains tax.

Capital gains tax can be of two types – long-term capital gains tax and short-term capital gains tax. The application of either of these types depends on the period for which you held the asset, after purchase, before transferring it and earning a gain on such a transfer.

Capital gains tax forms a part of your income tax computation and is calculated under the head ‘Income from Capital Gains’.

Besides these taxes, Wealth Tax and Gift Tax also formed a part of direct taxes. However, these taxes were abolished in the past years to make direct taxation a simpler affair.

Calculation of income tax

As stated earlier, income tax is the primary type of direct tax that affects you, the taxpayer. So, let’s understand how income tax is calculated on your income.

Firstly, there are five heads of income that, together, constitute your gross taxable income

- Income from salary

- Income from business or profession

- Income from capital gains

- Income from house property

- Income from other sources

All your income is segregated into these heads and then, collectively, apportioned to income tax.

The tax slabs for calculating the tax liability for individual taxpayers aged below 60 years and HUFs is as follows

| Level of income | Tax payable |

| Up to INR 250,000 | Nil |

| INR 250,001 to INR 500,000 | 5% of income exceeding INR 250,000 (However, if your taxable income is limited to INR 5 lakhs, you can claim a rebate on your tax liability under Section 87A. This rebate makes your tax liability nil) |

| INR 500,001 to INR 10,00,000 | INR 12,500 + 20% of income exceeding INR 500,000 |

| INR 10,00,001 and above | INR 112,500 + 30% of income exceeding INR 10,00,000 |

For senior citizens, the tax slab is as follows

| Level of income | Tax payable |

| Up to INR 300,000 | Nil |

| INR 300,001 to INR 500,000 | 5% of income exceeding INR 300,000 (However, if your taxable income is limited to INR 5 lakhs, you can claim a rebate on your tax liability under Section 87A. This rebate makes your tax liability nil) |

| INR 500,001 to INR 10,00,000 | INR 10,000 + 20% of income exceeding INR 500,000 |

| INR 10,00,001 and above | INR 110,000 + 30% of income exceeding INR 10,00,000 |

For super senior citizens, the slab is as follows

| Level of income | Tax payable |

| Up to INR 500,000 | Nil |

| INR 500,001 to INR 10,00,000 | 20% of income exceeding INR 500,000 |

| INR 10,00,001 and above | INR 100,000 + 30% of income exceeding INR 10,00,000 |

You can also claim exemptions and deductions under various sections of the Income Tax Act, 1961 to reduce your taxable income which, in turn, reduces your tax liability.

Let’s understand with examples

Example 1

Say you earn the following in a financial year

- Income from salary – INR 7 lakhs

- Rental income from house property – INR 2 lakhs

Moreover, you have invested in Section 80C avenues and have a deduction of INR 1.5 lakhs

Tax would be calculated as follows

| Income from salary | INR 7 lakhs |

| Income from house property (rental income) | INR 2 lakhs |

| Total income | INR 9 lakhs |

| Less: deduction available under Section 80C | INR 1.5 lakhs |

| Taxable income | INR 7.5 lakhs |

| Tax payable: Up to INR 2.5 lakhs INR 2.5 lakhs to INR 5 lakhs INR 5 lakhs to INR 7.5 lakhs | Nil 5% of INR 2.5 lakhs = INR 12,500 12500 + 20% of INR 2.5 lakhs = INR 62,500 |

So, you would have to bear a tax liability of INR 62,500 on the income that you have earned in the financial year.

Example 2

Mr Sharma finances in a financial year are as follows

- Income from the profession – INR 5 lakhs

- Income from capital gains – INR 1 lakh

- Deduction available under Section 80C – INR 1.5 lakhs

The tax would be calculated as follows

| Income from profession | INR 5 lakhs |

| Income from capital gains | INR 1 lakh |

| Total income | INR 6 lakhs |

| Less: Section 80C deductions | INR 1.5 lakhs |

| Taxable income | INR 4.5 lakhs |

| Tax payable | 5% of INR 2 lakhs = INR 10,000 |

| Less: Rebate available under Section 87A | INR 10,000 |

| Tax payable | Nil |

Since Mr Sharma’s taxable income was under INR 5 lakhs, he claimed a rebate of INR 10,000 and his tax liability became nil.

Types of indirect taxes in India

Like direct taxes, indirect taxes are of different types. These are as follows

- GST

Short for the Goods and Services Tax, GST was implemented from 1st July 2017 and it replaced all other forms of indirect taxes applicable on goods and services like sales tax, VAT, etc. GST became a unified tax and is not applicable on most goods and services that you purchase. - Toll tax

This tax is applicable if you travel interState or intraState. This tax is levied to allow you to pass from one area to another. - Road tax

Applicable for running a vehicle in India, this tax is applicable if you buy a two-wheeler or a four-wheeler. - Customs duty

This tax is applicable for moving goods between international borders. So, if you buy goods in another country and then bring such goods to India, customs duty would be payable on the value of such goods if such value exceeds specified limits.

A look into the Goods and Services Tax

Introduced in the year 2017, GST is a unified indirect tax that is applicable to goods and services. GST is divided into three parts

- State GST or SGST that is levied by States

- Central GST or CGST that is levied by the Central Government

- Integrated GST or IGST that is also levied by the Central Government

GST is applicable at each level of the sale of goods and services. Moreover, it helps in removing the cascading effect of different types of taxes and makes for a uniform and smoother taxation on goods and services. GST rates are different on different types of goods and services. The rates start from 0% and go up to 28%.

Methods to save tax in India

There are various ways in which you can reduce your tax liability by claiming exemptions and eligible deductions on your taxable income. Here are some ways of reducing taxes

- Using Section 80C deduction fully

Section 80C of the Income Tax Act, 1961 allows deductions up to INR 1.5 lakhs on eligible investments and expenses incurred in a financial year. Some of the avenues that allow deduction under Section 80C include the following- Life insurance premiums

- Investment in ELSS schemes

- Investment in NSC, SSY, KVP, SCSS schemes

- EPF and PPF contributions

- Investment into the NPS scheme

- Repayment of the principal component of a home loan

- Registration and stamp duty paid on a house property

- Tuition fees paid for children

- Using Section 80D

The benefit of this section is available if you invest in a health insurance policy. Premiums paid for the policy would be allowed as a deduction up to INR 25,000. The limit becomes INR 50,000 if you are a senior citizen. Moreover, if you also pay the premium for your parents’ health plan, you can claim an additional deduction up to INR 25,000 or INR 50,000 depending on the age of your parents. - Home loan benefits

Besides the principal repayment, the home loan interest is also allowed as an exempted expense under Section 24(b). You can claim a deduction of up to INR 2 lakhs on home loan interest paid during a financial year. Moreover, if you are a first time home buyer and you fulfil other conditions specified under Section 80EEA, you can claim an additional deduction of up to INR 1.5 lakhs on home loan interest paid during the financial year.

So, understand what taxation in India is all about and use these avenues to reduce your taxable liability by the maximum possible amount.

FAQ’s

Income tax is payable online through the portal of the income tax department. You can calculate and file your taxes online on the portal.

If an excess tax has already been paid on your behalf through TDS, you can file for an income tax refund. For this, you would have to file your income tax returns showing the tax liability vis-à-vis the TDS already paid. Thereafter, the income tax department would refund the excess tax paid on your behalf.

No, sales tax has been replaced by GST. So, now, if you buy any goods or services, you would only have to pay an additional GST on your purchase.

Yes, tax evasion is a serious offence. If you are found to evade your tax liability you would incur considerable penalties and might also suffer legal consequences.

Yes, you can claim as many deductions and exemptions on your taxable income as you can if you are eligible for the same.